The Power of Personal Loans

In India, where unforeseen expenses can arise anytime, personal loans offer a convenient way to bridge financial gaps. Whether it’s a medical emergency, home renovation, or debt consolidation, personal loans provide quick access to funds. But before applying, understanding your credit score and its role in the approval process is crucial.

Why Credit Score Matters

Your credit score, typically calculated by credit bureaus like CIBIL, is a three-digit number reflecting your creditworthiness. It’s a crucial factor influencing:

- Loan Approval: A good credit score significantly increases your chances of getting a personal loan approved.

- Interest Rates: Lenders offer lower interest rates to borrowers with high credit scores. This can save you a substantial amount of money over the loan repayment period.

- Loan Amount: A strong credit score may allow you to qualify for a higher loan amount, fulfilling your financial needs more effectively.

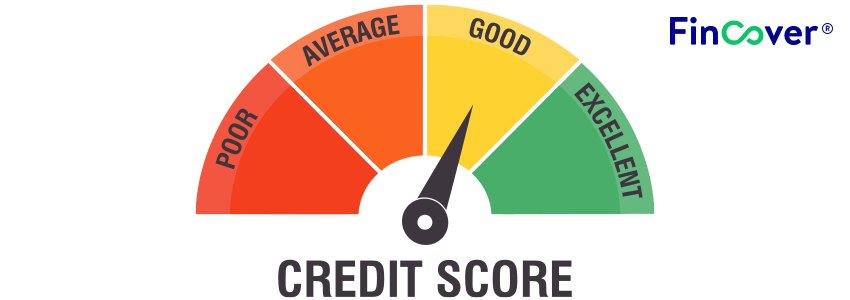

Demystifying Credit Score Requirements

While there’s no universally set minimum credit score for personal loans in India, lenders typically have their own benchmarks. Here’s a general guideline:

- Ideal Credit Score (750 and Above): This score signifies excellent creditworthiness, making you highly attractive to lenders and potentially qualifying you for the most favorable terms – fast approvals, competitive interest rates, and potentially higher loan amounts.

- Good Credit Score (700-749): This range indicates responsible credit management and can still lead to loan approvals, but interest rates and other terms may be less advantageous.

- Average Credit Score (650-699): While you may still secure a loan under this range, lenders may impose stricter eligibility criteria and offer less favorable terms.

- Below Average Credit Score (Below 650): Securing a personal loan with a score below 650 becomes challenging. Approval may be conditional or come with significantly higher interest rates and stricter terms.

Understanding Why Credit Score Matters

Your credit score tells lenders how responsible you are with managing debt. A good score indicates you’re a reliable borrower who makes timely payments. Conversely, a low score suggests a higher risk of missed payments or defaults, making lenders hesitant to offer you a loan or charging higher interest rates to compensate for the perceived risk.

Factors Affecting Your Credit Score

Several factors influence your credit score, including:

- Repayment History: Consistent on-time payments for credit cards, loans, and other debts significantly improve your score.

- Credit Utilization Ratio: This is the percentage of your credit limit you’re using. Aim to keep it below 30% for a positive impact on your score.

- Credit Mix: Having a healthy mix of secured loans (e.g., car loans) and unsecured loans (e.g., credit cards) can demonstrate responsible credit management.

- Credit Inquiries: Excessive credit inquiries within a short period can negatively impact your score. Apply for loans only when necessary.

Boosting Your Credit Score for a Personal Loan

Here are some steps you can take to improve your credit score and increase your chances of securing a favorable personal loan:

- Pay Bills on Time: This is the single most significant factor influencing your score. Make all your debt payments on or before the due date.

- Monitor Your Credit Report: Regularly review your credit report for errors and dispute any inaccuracies promptly. A clean and accurate report strengthens your creditworthiness.

- Become an Authorized User: Consider becoming an authorized user on someone else’s credit card with a good payment history. Their positive payment behavior can improve your score over time.

- Practice Responsible Borrowing: If you already have credit cards or loans, use them responsibly and pay your balances in full whenever possible.

Beyond Credit Score: Additional Considerations

While your credit score is crucial, here are some other factors lenders may consider when evaluating your personal loan application:

- Employment Status: Stable employment history demonstrates consistent income to repay the loan.

- Income Level: Your income level should be sufficient to cover your monthly expenses and potential loan payments comfortably.

- Debt-to-Income Ratio (DTI): A high DTI indicates a significant existing debt burden, potentially making lenders hesitant to offer you another loan.

- Loan Purpose: Some lenders may offer personalized interest rates or loan terms depending on the specific purpose of your personal loan.

Seeking Professional Guidance:

If you’re unsure about your creditworthiness or need assistance navigating the personal loan application process, consider consulting:

- Financial Advisor: A qualified financial advisor can assess your financial situation, recommend strategies to improve your credit score, and help you choose the right personal loan options based on your needs and goals.

- Loan Specialist: A loan specialist from a bank or lending institution can provide insights into their specific credit score requirements and loan programs, guiding you towards the best option for your circumstances.

Conclusion

Understanding credit score requirements and taking proactive steps to improve your score are crucial steps towards securing a personal loan and managing unforeseen financial needs with ease. Remember, a good credit score empowers you to access better loan terms, potentially saving you significant money on interest payments. By following the tips outlined in this blog and seeking professional guidance when needed, you can navigate the world of personal loans with confidence and unlock greater financial flexibility to navigate life’s unexpected challenges.