The Power of Credit Score in Business Loan Eligibility

In India, your business credit score, often calculated by CIBIL, acts as a vital indicator of your financial health and creditworthiness. It plays a significant role in determining:

- Loan Approval: A strong credit score significantly increases your chances of getting a business loan approved.

- Loan Terms: Lenders offer better loan terms, including lower interest rates and longer repayment periods, to businesses with good credit scores.

- Loan Amount: A higher credit score may enable you to qualify for a larger loan amount, allowing you to invest in your business growth plans more effectively.

Understanding Credit Score Benchmarks

While there’s no universally set minimum credit score for business loans in India, lenders typically have their own benchmarks, which can vary depending on several factors, including:

- Loan Type: Different loan types, such as term loans, working capital loans, or equipment financing, may have varying credit score requirements.

- Loan Amount: Loans for larger amounts may necessitate a higher credit score compared to smaller loans.

- Industry: Credit score expectations might differ across various industries based on the perceived risk associated with each sector.

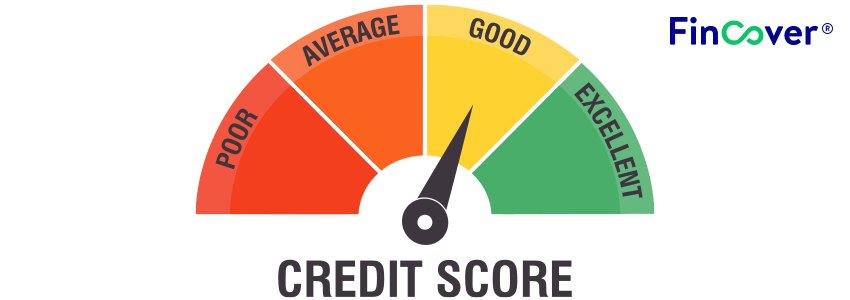

General Credit Score Benchmarks

Here’s a general guideline based on CIBIL scores:

- Ideal Credit Score (750 and Above): This score signifies strong financial health and credit management, making your business highly attractive to lenders and potentially qualifying you for the most favorable loan terms.

- Good Credit Score (700-749): This range indicates responsible credit behavior and can still lead to loan approvals, but interest rates and other terms may be less advantageous.

- Average Credit Score (650-699): While you may still secure a loan under this range, lenders might impose stricter eligibility criteria and offer less favorable terms.

- Below Average Credit Score (Below 650): Securing a business loan with a score below 650 becomes challenging. Approval may be conditional or come with significantly higher interest rates and stricter terms.

Why Credit Score Matters

Your business credit score reflects your ability to manage financial obligations responsibly. A good score indicates to lenders that your business is a reliable borrower, likely to repay the loan on time and in full. Conversely, a low credit score suggests a higher risk of default, making lenders hesitant to offer you a loan or charging higher interest rates to compensate for the perceived risk.

Factors Affecting Your Business Credit Score

Several factors influence your business credit score, including:

- Business Payment History: Timely repayments for previous loans, vendor invoices, and other business-related debts significantly improve your score.

- Credit Inquiries: Excessive credit inquiries within a short period can negatively impact your score. Seek loans only when necessary for your business needs.

- Public Records: Negative events like judgments or liens against your business can adversely affect your credit score.

- Financial Performance: Lenders may consider your business’s financial statements, like income statements and balance sheets, to assess its financial health and stability.

Improving Your Business Credit Score

Here are some strategies to improve your business credit score and increase your chances of securing a favorable business loan:

- Establish Business Credit: Build a positive business credit history by obtaining a business credit card or loan and making timely payments.

- Maintain a Healthy Credit Mix: Utilize a mix of credit products, such as business loans and credit lines, to demonstrate responsible credit management.

- Monitor Your Business Credit Report: Regularly review your business credit report for errors and dispute any inaccuracies promptly. A clean and accurate report strengthens your creditworthiness.

- Practice Responsible Borrowing: Only borrow what your business requires and ensure you can comfortably manage the loan repayments. Overextending your credit can negatively impact your score.

Additional Considerations Beyond Credit Score

While your credit score is an essential factor, lenders also consider other aspects when evaluating your business loan application:

- Business Plan: A well-defined and comprehensive business plan outlining your financial projections, growth strategies, and market understanding demonstrates your entrepreneurial potential and the viability of your business.

- Collateral: Depending on the loan type and lender, you may need to offer collateral, such as property or equipment, to secure the loan. This acts as additional security for the lender if you default on the loan.

- Industry Experience and Track Record: A proven track record of success in your industry fosters confidence in lenders regarding your ability to manage the loan effectively.

Seeking Professional Guidance:

Navigating the business loan landscape can be complex. Consider seeking guidance from the following professionals:

- Financial Advisor: A qualified financial advisor can assess your business’s financial health, recommend strategies to improve your credit score, and help you choose the most suitable loan options based on your needs and goals.

- Business Loan Specialist: A lender-specific business loan specialist can provide insights into their specific credit score requirements and loan programs, helping you tailor your application for optimal chances of approval.

Conclusion:

Understanding credit score requirements and taking proactive steps to improve your business credit score are crucial steps towards securing a business loan and fueling your entrepreneurial aspirations. Remember, a good credit score empowers you to access better loan terms, potentially saving your business significant financial resources. By following the tips outlined in this blog and seeking professional guidance when needed, you can navigate the world of business loans with confidence and unlock the doors to greater growth and success for your venture